Comparing Travel Insurance Policies for International Trips

Choose the right travel insurance for your international adventures. Compare coverage, benefits, and providers.

Choose the right travel insurance for your international adventures. Compare coverage, benefits, and providers.

Comparing Travel Insurance Policies for International Trips

Hey there, fellow globetrotter! So, you've got your flights booked, your accommodation sorted, and your itinerary packed with exciting adventures. But wait, have you thought about travel insurance? I know, I know, it's not the most glamorous part of planning a trip, but trust me, it's one of the most crucial. Think of it as your safety net, your peace of mind, your superhero cape against unexpected travel mishaps. Whether you're planning a relaxing beach getaway, an adrenaline-fueled mountain trek, or a cultural immersion in a bustling city, things can go wrong. Flights get delayed, luggage goes missing, and unfortunately, people get sick or injured. That's where travel insurance swoops in to save the day.

But with so many options out there, how do you even begin to choose? It can feel like navigating a maze of jargon and fine print. Don't sweat it! This guide is here to help you compare travel insurance policies for international trips, breaking down the key aspects you need to consider. We'll look at different types of coverage, what to watch out for, and even recommend some popular providers to get you started. Let's dive in!

Understanding Travel Insurance Coverage Types What Does Travel Insurance Cover

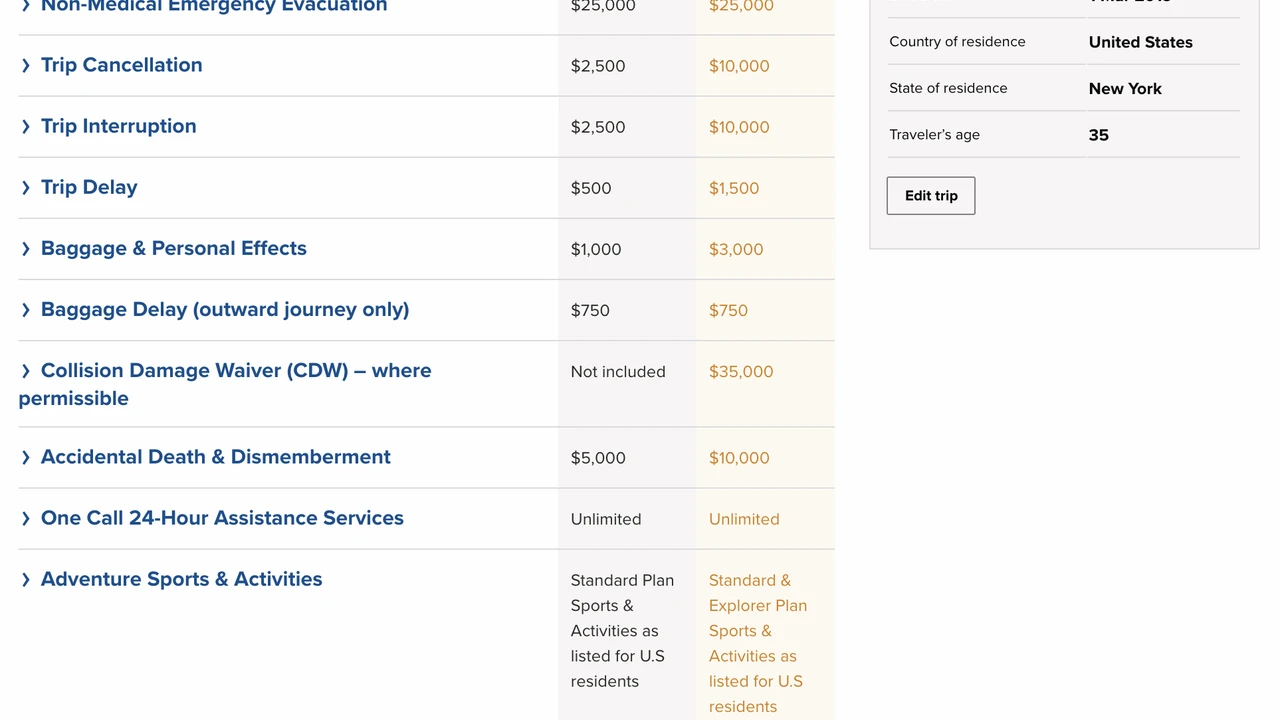

First things first, let's talk about what travel insurance actually covers. It's not a one-size-fits-all kind of deal, and policies can vary significantly. However, most comprehensive plans will offer a combination of the following:

Medical Emergencies and Evacuation Travel Medical Insurance

This is arguably the most important part of any travel insurance policy, especially for international trips. Imagine getting seriously ill or injured in a foreign country. Medical bills can skyrocket, and getting transported back home can cost a fortune. Medical emergency coverage typically includes:

- Emergency Medical Treatment: Covers doctor visits, hospital stays, surgeries, and prescription medications.

- Emergency Medical Evacuation: If you need to be transported to a better-equipped medical facility or back to your home country for treatment, this covers the costs. This can be incredibly expensive without insurance.

- Repatriation of Remains: In the unfortunate event of death, this covers the costs of returning remains home.

Key things to look for: High coverage limits (at least $100,000, but ideally more for international travel), coverage for pre-existing conditions (often with specific clauses), and a 24/7 emergency assistance hotline.

Trip Cancellation and Interruption Protecting Your Travel Investment

Life happens, and sometimes, despite your best efforts, you have to cancel or cut short your trip. This coverage protects your financial investment in non-refundable expenses.

- Trip Cancellation: Reimburses you for non-refundable expenses (flights, hotels, tours) if you have to cancel your trip before it starts due to covered reasons (e.g., illness, injury, death in the family, natural disaster at your destination).

- Trip Interruption: Reimburses you for the unused portion of your trip and often covers additional costs to return home if your trip is cut short due to a covered reason.

Key things to look for: A clear list of covered reasons for cancellation/interruption, and sufficient coverage to cover all your non-refundable pre-paid expenses.

Baggage Loss Delay and Damage Luggage Protection

Lost luggage is a traveler's nightmare. This coverage helps ease the pain.

- Baggage Loss/Theft: Reimburses you for the value of your lost, stolen, or damaged luggage and its contents.

- Baggage Delay: Provides a stipend to purchase essential items (toiletries, clothes) if your luggage is delayed for a certain period (e.g., 6-12 hours).

Key things to look for: Adequate per-item limits (especially for electronics or valuables), and a reasonable delay period before coverage kicks in.

Travel Delay and Missed Connections Flight Delay Coverage

Delays are an inevitable part of travel. This coverage can help mitigate the financial impact.

- Travel Delay: Reimburses you for additional expenses (meals, accommodation) if your trip is delayed for a specified number of hours due to a covered reason (e.g., mechanical breakdown, severe weather).

- Missed Connection: Covers additional costs to catch up to your itinerary if you miss a connecting flight due to a delay of a previous flight.

Key things to look for: A reasonable delay threshold (e.g., 3-6 hours) and sufficient daily limits for expenses.

Rental Car Damage Protection Car Rental Insurance

If you plan on renting a car abroad, this can be a valuable addition. It typically covers damage to the rental vehicle due to collision, theft, or vandalism. This can often be a cheaper alternative to the insurance offered by rental car companies.

Comparing Travel Insurance Providers Top Travel Insurance Companies

Now that you know what to look for, let's talk about some popular travel insurance providers. Remember, it's always best to get quotes from several companies and compare their policies side-by-side.

World Nomads Adventure Travel Insurance

Who it's for: Backpackers, adventure travelers, and those who might extend their trips. World Nomads is known for its flexibility and coverage for a wide range of adventure activities.

Key Features:

- Adventure Activities: Covers over 200 adventure activities, from bungee jumping to scuba diving.

- Extend Your Policy: You can extend your policy online while still traveling.

- Emergency Medical: Strong medical coverage, including evacuation.

- Gear Protection: Good coverage for electronics and sports equipment.

Potential Drawbacks: Can be slightly more expensive than basic policies if you don't need adventure coverage. Pre-existing conditions coverage might be limited.

Example Scenario: You're trekking in Nepal and twist your ankle. World Nomads would cover your medical treatment and potentially your evacuation to a better hospital. Or, you decide to spontaneously add a week in Thailand; you can extend your policy on the go.

Typical Price Range: For a 2-week trip to Southeast Asia for a 30-year-old, a standard policy might range from $80-$150, depending on the level of coverage and activities included.

Allianz Travel Insurance Reliable Travel Protection

Who it's for: Travelers looking for comprehensive coverage from a well-established provider. Allianz offers a variety of plans, from basic to premium, catering to different needs.

Key Features:

- Variety of Plans: Offers single-trip, annual, and rental car insurance plans.

- 24/7 Assistance: Excellent customer service and emergency assistance.

- Good for Families: Often has good options for family coverage.

- Optional Add-ons: Can add coverage for things like 'Cancel Anytime' (though this is usually expensive and has specific conditions).

Potential Drawbacks: Some plans might have lower limits for baggage or specific activities compared to specialist providers. 'Cancel Anytime' is often not as comprehensive as it sounds.

Example Scenario: Your flight to Europe is delayed by 8 hours due to a mechanical issue. Allianz would cover your meals and accommodation during the delay. Or, you have to cancel your trip last minute because a family member falls ill; your non-refundable expenses would be reimbursed.

Typical Price Range: For a 2-week trip to the USA for a 30-year-old, a comprehensive plan might range from $100-$200, depending on the level of coverage and any add-ons.

SafetyWing Nomad Insurance Digital Nomad Insurance

Who it's for: Digital nomads, long-term travelers, and those who need flexible, subscription-based insurance that can be purchased while already abroad.

Key Features:

- Subscription Model: Pay monthly, similar to a subscription service, and cancel anytime.

- Can Purchase While Traveling: Great for spontaneous trips or if you forgot to buy insurance before leaving.

- Home Country Coverage: Includes limited coverage in your home country for short periods.

- Good for Long-Term: Designed for extended trips and remote workers.

Potential Drawbacks: Lower coverage limits for some benefits compared to traditional comprehensive plans. Not ideal for short, expensive trips where high cancellation coverage is needed. Deductibles can be higher.

Example Scenario: You're a digital nomad living in Thailand and decide to take a spontaneous trip to Vietnam. You can easily add SafetyWing coverage for your new destination. Or, you get a minor illness while abroad; SafetyWing would cover your doctor's visit.

Typical Price Range: Around $45-$60 per 4 weeks, depending on age and destination. This is a monthly subscription, so it's different from a single-trip policy.

Travelex Insurance Services Comprehensive Travel Plans

Who it's for: Travelers looking for a range of comprehensive plans with good customer service and options for various budgets.

Key Features:

- Multiple Plan Tiers: Offers different levels of coverage (e.g., Travel Select, Travel Basic) to suit various needs and budgets.

- Optional Upgrades: Can add 'Cancel For Any Reason' (CFAR) or adventure sports coverage.

- Good Customer Support: Known for responsive customer service.

Potential Drawbacks: CFAR is an expensive add-on and usually only reimburses a percentage (e.g., 50-75%) of your non-refundable costs. Some plans might have lower medical limits than others.

Example Scenario: You've booked an expensive cruise and want the option to cancel for any reason, even if it's just a change of heart. Travelex's CFAR add-on could provide some reimbursement. Or, you need robust medical coverage for a trip to a country with high medical costs.

Typical Price Range: For a 2-week trip to Europe for a 30-year-old, a comprehensive plan might range from $90-$180, depending on the level of coverage and any add-ons.

Key Considerations When Choosing Travel Insurance What to Look For

Beyond comparing providers, here are some crucial factors to keep in mind when making your final decision:

Pre Existing Medical Conditions Travel Insurance for Health Issues

If you have any pre-existing medical conditions (e.g., diabetes, heart disease, asthma), this is a big one. Many policies have clauses that exclude coverage for these conditions unless you meet specific criteria, often involving purchasing the policy within a certain timeframe of your initial trip deposit and being medically stable. Always declare any pre-existing conditions and read the fine print carefully.

Adventure Activities and Sports Coverage Extreme Sports Insurance

Planning to go scuba diving, skiing, rock climbing, or bungee jumping? Many standard policies exclude these 'hazardous' activities. If you're an adrenaline junkie, you'll need a policy that specifically covers your chosen activities. Providers like World Nomads are often a good choice here, or you might need to add an adventure sports rider to a standard policy.

Coverage Limits and Deductibles Understanding Your Policy

Don't just look at the headline price. Dig into the coverage limits for each benefit (e.g., $100,000 for medical, $500 for lost baggage per item). Also, check the deductible – this is the amount you have to pay out of pocket before your insurance kicks in. A higher deductible usually means a lower premium, but it also means you'll pay more if you make a claim.

Policy Exclusions What Travel Insurance Does Not Cover

Just as important as what's covered is what's NOT covered. Common exclusions include:

- Acts of War or Terrorism: Though some policies offer limited coverage.

- Self-Inflicted Injuries: Injuries sustained while under the influence of drugs or alcohol.

- Elective Procedures: Cosmetic surgery or non-emergency treatments.

- High-Risk Activities: Unless specifically added.

- Negligence: If you leave your bag unattended and it's stolen.

- Changing Your Mind: Unless you have 'Cancel For Any Reason' coverage, which is usually an expensive add-on.

Always read the policy wording carefully to understand the exclusions.

Customer Service and Emergency Assistance 24/7 Support

When you're in a foreign country and facing an emergency, you want to know you can get help quickly. Look for providers with 24/7 emergency assistance hotlines and good customer reviews regarding their claims process. A responsive and helpful support team can make a huge difference in a stressful situation.

Cost and Value Finding Affordable Travel Insurance

While cost is a factor, don't let it be the only one. The cheapest policy might leave you underinsured when you need it most. Get multiple quotes, compare the benefits and limits, and choose a policy that offers good value for your specific trip and needs. Sometimes, paying a little extra upfront can save you a lot of money and stress down the line.

Tips for Buying Travel Insurance Smart Travel Insurance Choices

To make sure you're getting the best deal and the right coverage, here are a few pro tips:

Buy Early for Maximum Protection Early Bird Travel Insurance

Purchase your travel insurance as soon as you make your first non-refundable trip deposit (e.g., flight or hotel). This is especially important for trip cancellation coverage and for qualifying for pre-existing condition waivers.

Read the Fine Print Policy Wording Explained

I know it's boring, but seriously, read the policy document. Understand what's covered, what's excluded, and what the claims process entails. If anything is unclear, contact the insurance provider for clarification.

Consider Annual Multi Trip Policies Frequent Traveler Insurance

If you travel frequently (e.g., more than 2-3 times a year), an annual multi-trip policy might be more cost-effective than buying individual policies for each trip. These policies cover all your trips within a 12-month period, usually up to a certain duration per trip.

Check Your Existing Coverage Credit Card Travel Benefits

Some premium credit cards offer basic travel insurance benefits, such as trip delay, baggage delay, or even rental car insurance. Check with your credit card provider to see what's included. However, these benefits are often secondary (meaning they kick in after your primary insurance) and might have lower limits than a dedicated travel insurance policy. Don't rely solely on credit card coverage for major medical emergencies.

Document Everything Claims Process Documentation

In the unfortunate event that you need to make a claim, documentation is key. Keep copies of all your travel documents (tickets, itineraries, booking confirmations), receipts for any expenses incurred due to delays or cancellations, medical reports, police reports (for theft), and communication with airlines or tour operators. The more evidence you have, the smoother the claims process will be.

Real World Scenarios Why Travel Insurance Matters

Let's look at a couple of scenarios to really drive home why travel insurance is a non-negotiable for international trips:

Scenario 1 Unexpected Illness Abroad

You're enjoying a delicious street food tour in Vietnam, but a few days later, you come down with a severe case of food poisoning. You need to see a doctor, and it turns out you require a few days in a local hospital for IV fluids and observation. Without travel insurance, this could easily cost you thousands of dollars out of pocket, not to mention the stress of navigating a foreign medical system. With a good policy, your medical bills are covered, and the 24/7 assistance line can help you find a reputable hospital and even arrange translation services.

Scenario 2 Lost Luggage and Missed Connection

You're flying from London to Bangkok with a tight connection in Dubai. Your first flight is delayed by 4 hours due to an unexpected mechanical issue. You miss your connecting flight to Bangkok, and your checked luggage doesn't make it either. Without insurance, you're stuck paying for a new flight, a night in a hotel in Dubai, and new clothes and toiletries until your bag arrives (which could be days!). With travel insurance, your policy would cover the cost of the new flight, your accommodation and meals during the delay, and provide a stipend to buy essential items until your luggage is found.

See? It's not just about the big, scary emergencies. Travel insurance can also save you from the smaller, but equally frustrating, inconveniences that can derail your trip and your budget.

So, there you have it! Comparing travel insurance policies for international trips doesn't have to be a headache. By understanding the different types of coverage, knowing what to look for in a provider, and keeping these tips in mind, you can confidently choose a policy that protects you and your travel investment. Don't leave home without it!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)